Income taxes are the most visible, but they are far from the only taxes you pay. A complete picture of your tax burden includes several other types.

Capital gains taxes apply when you sell an investment – a stock, a fund or a piece of real estate – for more than you paid. The rate depends on how long you held the investment. Assets held more than one year are generally taxed at a lower, preferential rate; assets held one year or less are taxed at your ordinary income rate.

Sales taxes are charged on goods and services you purchase. Property taxes are assessed on real estate and, in some jurisdictions, on cars, boats and other assets. Gift taxes may apply when you give money or assets to another person above a certain annual limit. And estate or death taxes apply to the total value of your estate above an applicable exemption amount when you die.

Understanding that taxes show up at every stage of your financial life – when you earn, spend, invest and transfer wealth – is the foundation of sound financial planning. One useful way to think about it: it’s not what you earn that counts; it’s what you keep after taxes.

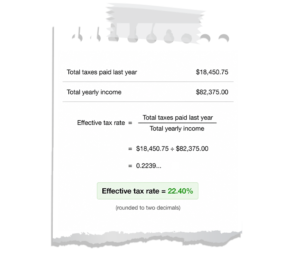

People often confuse their marginal tax rate with their effective tax rate. Your marginal rate is the rate that applies to each additional dollar of income. Your effective rate is what you actually pay on your total income.

People often confuse their marginal tax rate with their effective tax rate. Your marginal rate is the rate that applies to each additional dollar of income. Your effective rate is what you actually pay on your total income.