Personal Finance Essentials

The Cost of Waiting: Why Starting Early Matters

- Back to Retirement Planning

- The Key Challenge in Retirement Planning

- A Brief History of Retirement

- How Much You Need to Save

- The Cost of Waiting: Why Starting Early Matters

- Workplace Retirement Plans

- Individual Retirement Accounts

- Investing Your Retirement Savings

- Required Minimum Distributions

- Generating Income in Retirement

- Long-Term Care Planning

- Disability Insurance: Protecting Your Income

- Managing Retirement Accounts Through Life Changes

- College Savings and Retirement: Getting the Balance Right

- Estate Planning for Retirement Accounts

- Common Mistakes to Avoid

- Retirement as a Family Affair

- Planning the Life You Want in Retirement

One Year of Delay Costs You $70,000

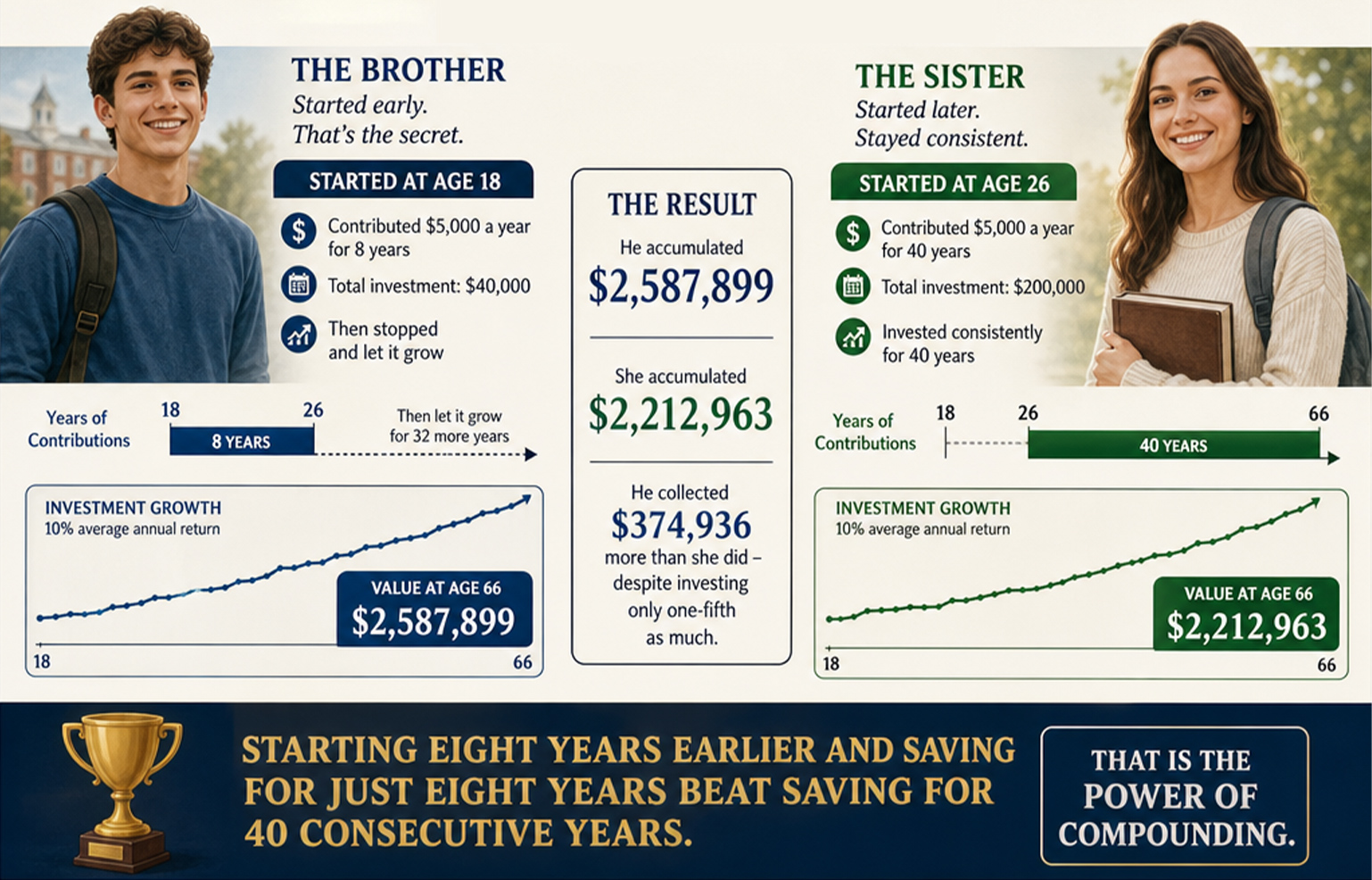

Eight Years of Delay Costs You Nothing — If You Start at 18

Consider the story of a brother and sister. At age 18, he contributed $5,000 a year to an IRA for eight years and then stopped – a total investment of $40,000. His sister started at age 26 and contributed $5,000 a year for 40 consecutive years – a total of $200,000. Both earned a 10% annual return.

The result: she accumulated $2,212,963. He collected $2,587,899 – $374,936 more than she did – despite investing only one-fifth as much. Starting eight years earlier and saving for just eight years beat saving for 40 consecutive years. That is the power of compounding.

Suppose you are 30 years old.

Workers who continued investing in their 401(k) plans throughout the decade ending December 31, 2012 saw the size of their accounts quadruple, even though the S&P 500 Stock Index rose only 62% during that same period. You can grow your wealth no matter what the economy is doing – but only if you stay invested.