We’re entering an era where living past 100 will be common. Thanks to advances in medical technology, genetics and preventive health care, many people alive today are likely to see their 100th birthday and beyond.

This changes everything.

Living longer means rethinking the timeline of our lives. Instead of one long stretch of education, followed by one long career, followed by retirement, we’ll have multiple careers interspersed with extended sabbaticals, returns to school to learn new skills – and we’ll likely continue earning an income well into our 80s and 90s, partly because we’ll need the money and partly because we’ll want to stay engaged. Health care costs will remain a threat, as will inflation.

A longer life can be wonderful, but only if it’s financially sustainable. Planning for longevity isn’t just about building a bigger nest egg – it’s about giving you flexibility, so you can enjoy the life you want for many decades to come.

A longer life can be wonderful, but only if it’s financially sustainable. Planning for longevity isn’t just about building a bigger nest egg – it’s about giving you flexibility, so you can enjoy the life you want for many decades to come.

Life expectancy tables from the IRS, life insurers, the National Institutes of Health and the Centers for Disease Control and Prevention all point in the same direction: a 75-year-old today is expected to live to 87.4. An 85-year-old is expected to live to 91.7. And people who reach 100 are expected to live to 102.2. The older you are, the older you’re expected to get. Soon, half of all deaths in the U.S. will occur after age 80.

The catch is that nearly all of those tables assume life expectancies will remain at today’s levels. That is not likely. Research suggests people will continue to live longer and longer. In fact, even those as old as 45 today might still be alive in the 22nd century. Knowing that, most conservative financial planners now build plans that extend to age 95 or 100 – and for younger clients, that number is creeping higher still.

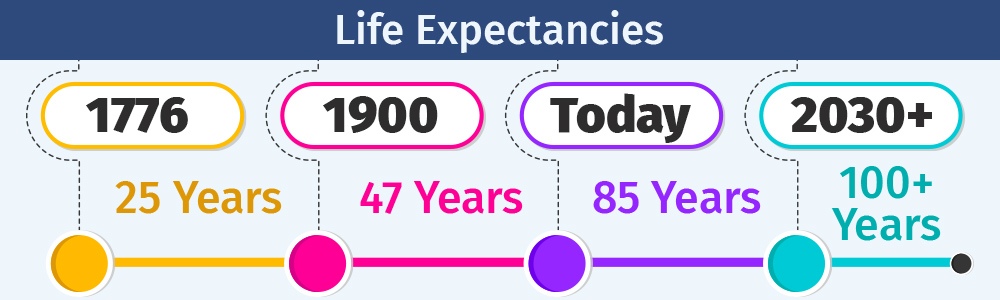

The traditional model of life – school, then career, then retirement – was designed for a world where most people died in their 60s. It no longer fits. When the Declaration of Independence was signed, life expectancy was just 25. Even in 1900, most Americans died by age 47. Retirement, as a concept, didn’t exist for most of human history: if you were alive, you worked.

That has changed dramatically. And as lifetimes extend further, the old model will continue to break down. We can already see it happening. Police officers, firefighters, teachers and government employees often become eligible for pensions before they turn 50. Most then enter entirely new careers. Some return to school at 69 to earn advanced degrees. Others start businesses in their 70s.

That has changed dramatically. And as lifetimes extend further, the old model will continue to break down. We can already see it happening. Police officers, firefighters, teachers and government employees often become eligible for pensions before they turn 50. Most then enter entirely new careers. Some return to school at 69 to earn advanced degrees. Others start businesses in their 70s.

If today’s trends continue, we may find that people in 2050 are marrying for the first time in their 50s, having children in their 60s, facing middle age in their 80s and retiring in their 120s. That may sound extreme – but given how dramatically the timeline has already shifted, it is not impossible.

A longer life almost certainly means multiple careers. The skills you develop in your 30s may be obsolete by your 50s. New industries will emerge. Others will disappear. People who plan for one career and one retirement will find themselves unprepared for the reality of a 100-year life.

A longer life almost certainly means multiple careers. The skills you develop in your 30s may be obsolete by your 50s. New industries will emerge. Others will disappear. People who plan for one career and one retirement will find themselves unprepared for the reality of a 100-year life.

Rites of passage will extend as well. As recently as 1960, marrying in your late teens was common. Today, the average age at first marriage has risen considerably, and it will continue to climb. Parenthood, homeownership and career milestones that once happened in a narrow band of years will become spread across decades. The concept of ‘old’ will keep shifting forward.

One statistic makes all of this vivid: U.S. Census research shows that 55 to 60 percent of women over 75 have been widows at some point, with a significant number remarrying. We are already a multiple-marriage society. As lifetimes extend, that will only become more so.