Debt is an important and unavoidable part of financial life. Without loans, most people could not buy a car or a home. Entrepreneurs could not start businesses. Governments could not fund infrastructure or provide services. Loans make it possible to achieve goals that would otherwise require decades of saving first. The key distinction is not between having debt and having none – it is between productive debt and destructive debt.

Debt is an important and unavoidable part of financial life. Without loans, most people could not buy a car or a home. Entrepreneurs could not start businesses. Governments could not fund infrastructure or provide services. Loans make it possible to achieve goals that would otherwise require decades of saving first. The key distinction is not between having debt and having none – it is between productive debt and destructive debt.

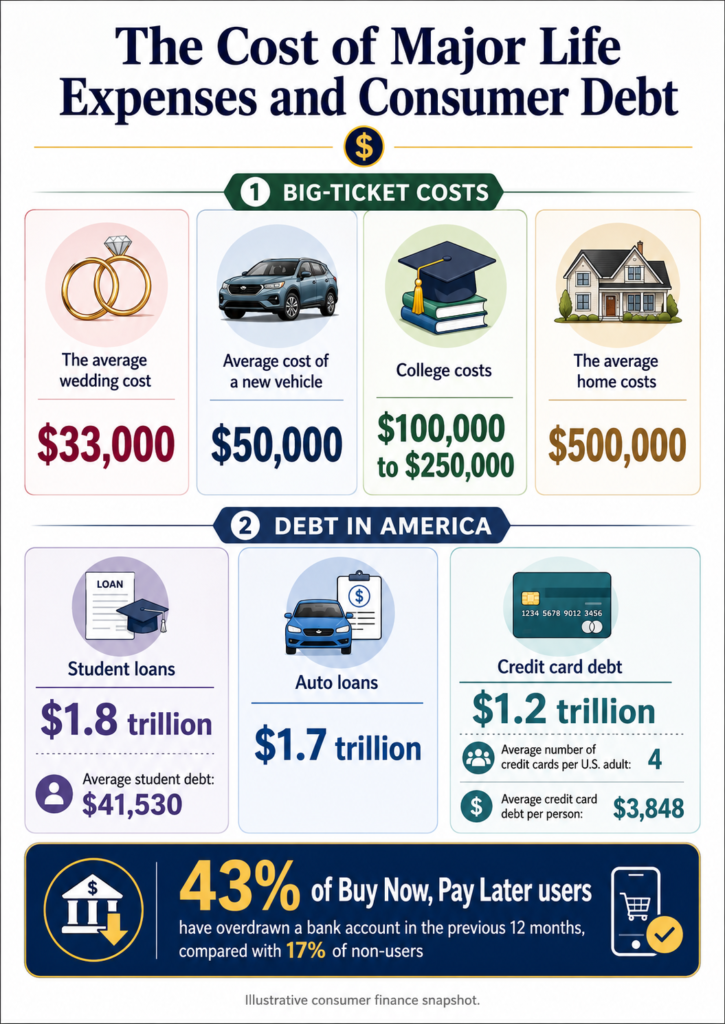

Productive debt finances assets that appreciate in value or generate income: a mortgage on a home, a student loan that leads to a higher-paying career, a business loan that funds growth. Destructive debt finances consumption: credit card balances that carry 18% to 25% interest, financing for depreciating assets like vehicles and buy-now-pay-later schemes that extend spending beyond current means. The rule is straightforward – only borrow what you can genuinely afford to repay, and only for purposes that justify the cost.

Many people fail at building wealth not because they lack income or discipline, but because they never defined what they were trying to accomplish. Without a goal, you cannot determine how much to save, what level of risk is appropriate, which investments to choose or how to measure whether you are making progress.

Setting a financial goal provides direction. Long-term goals – where the money will not be needed for decades – can tolerate more short-term volatility than near-term goals where funds will be needed soon. A retirement account invested for 30 years can ride out market downturns that would be catastrophic for money needed in two years. Goal-setting aligns your investment approach with your actual timeline.

Setting a financial goal provides direction. Long-term goals – where the money will not be needed for decades – can tolerate more short-term volatility than near-term goals where funds will be needed soon. A retirement account invested for 30 years can ride out market downturns that would be catastrophic for money needed in two years. Goal-setting aligns your investment approach with your actual timeline.

Goals also improve discipline. Markets rise and fall, sometimes dramatically. Without a clear goal to anchor your thinking, market volatility can trigger emotional reactions that lead to costly decisions – selling at bottoms, chasing recent winners and abandoning long-term plans at precisely the wrong moments. When you know what you are saving for and when you need it, short-term market movements become less threatening and less tempting to react to.

The most common financial goals people plan around include: buying a car, funding their own education, getting married, purchasing a home, raising children, funding their children’s college education, caring for aging parents, travel and experiences, and starting a business. Each of these carries its own price tag and timeline. A plan that accounts for all of them simultaneously – rather than addressing each one in isolation as it arrives – is the difference between a financial plan and a series of financial reactions.

Setting goals transforms investing from a vague, speculative activity into an intentional plan that is far more likely to deliver the results you want. It is not just the first step in financial planning. It is the step that makes all the other steps possible.